The UK electricity grid is becoming a major constraint on growth, with connection delays, ageing transformers and rising demand from renewables, battery storage, data centres and electrification putting the physical network under pressure. Hannah Willison argues that meeting Britain’s 2030 and 2035 energy targets will depend not just on policy reform, but on investment in the specialist SMEs building substations, manufacturing transformers and delivering the grid infrastructure needed to connect new capacity.

Near Aberthaw in Wales, there are developers facing a five-year wait to receive power despite sitting on a former coal site with seaside cooling water and a 1.5-gigawatt (‘GW’) connection already wired. For sites with no existing infrastructure, developers are looking at a decade. The electricity network stands between Britain and almost everything it wants to build next.

The National Grid Connection Queue has over 2,000 substations waiting in line – the largest with transformers at up to 400kV in size, capable of handling up to 2.5 GW of electricity or 25 million household light bulbs. To put that further into perspective, the smallest of substation-sized transformers are 132kV transformers with a fraction of capacity at only 0.12 GW – these weigh between 15 and 60 tons. Each one of those substations belongs to a generation or storage project hoping to plug into the system, all chasing a share of the roughly 283GW of capacity the UK says it needs by 2035 (132GW by 2030, rising to 151GW by 2035); somewhere in the region of three billion lightbulbs' worth of electricity.

How likely is this target to be met?

The question is not whether this capacity increase will happen – it has to – it’s a question of when. In order meet the 2030 – 2035 targets, over the next 10 years the UK electricity network needs to deliver twice the capacity of the last decade in half of the time.

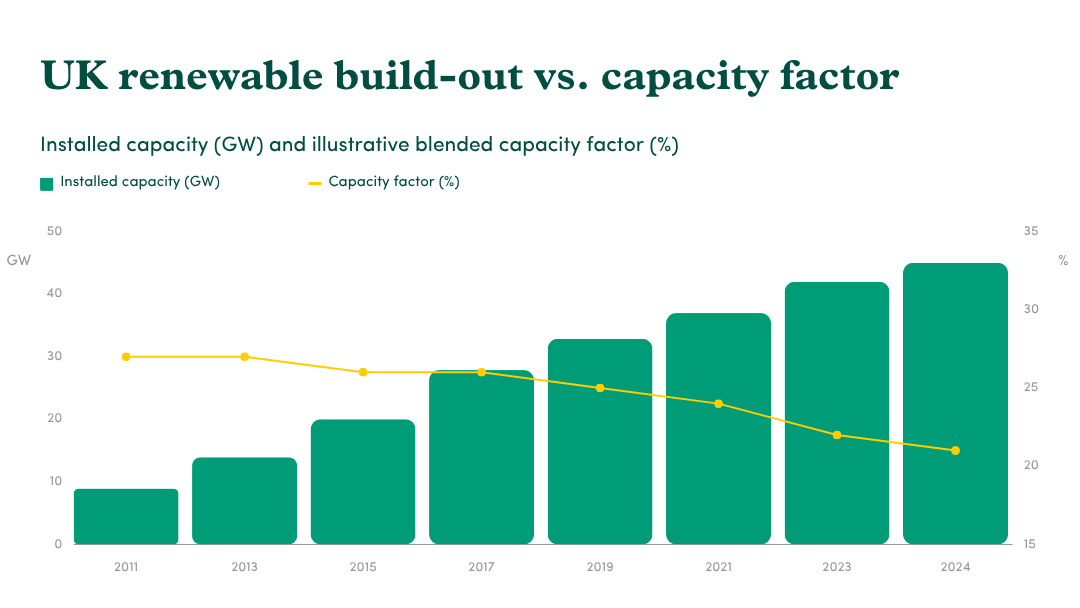

It's worth remembering how recent this problem is. Sixty years ago, Britain's grid was built around coal, then nuclear, then gas, which meant our network was powered by a handful of enormous, predictable power stations. What’s more, traditional sources of power run at high utilisation - a nuclear plant runs at something like a 75% capacity factor - and plug into a handful of points on the transmission network.

Renewables don't work like that. Offshore wind runs at around 38.7% capacity factor; solar at just 9.8%. The wind doesn't always blow, and the sun doesn't always shine. This means the grid needs far more connected capacity to deliver the same reliable amount of usable power. You also need that capacity sited near the wind or the sun, not necessarily near the substations or the demand that already exists. This problem shows up everywhere: the global energy mix is diversifying away from a few large, predictable plants, even as fossil fuels still make up the bulk of forecast global supply.

Layer on top of that the UK's ageing physical kit: the average transformer on the network is somewhere between 35 and 60 years old, against a recommended working life of 35 years. Add rising urgency to electrify transport and heating, and a geopolitical environment that's brought energy security to the forefront of political discourse, and the ask of the grid is trifold: diversify, modernise, and expand. Simultaneously, and at an unprecedented rate.

How will the power we need be brought online?

For the best part of twenty years, the dominant story about British electricity demand has been that it's falling: down around 22% since 2005, roughly 10% in the last decade alone, as the industry shrank and electrical efficiency improved. Grid planning, pricing, and investment have all been shaped by that downwards trade. This under-invested, aged grid dynamic is only recently juxtaposed against a future full of datacentres and wide-spread integration of AI into essential everyday life.

Frustratingly, while a meaningful share of the Connection Queue is genuinely new appetite across renewables, battery energy storage systems (‘BESS’), data centres, electrified heating and transport, there is a layer of complication through speculative noise. The dynamic is this: when a connection offer becomes increasingly scarce and valuable, the rational move for any developer is to apply early and often, "just in case," irrespective of whether the project gets built. This means the headline size of the demand queue should be read with scepticism, but this has to be balanced against a likely understated underlying need for more electrified demand, given how far consumption has fallen since 2005.

How does SME investing solve this problem?

The issues outlined above won’t get solved by NESO or Ofgem alone signing off bigger numbers. It gets solved, physically, by substations getting built, transformers getting manufactured, and connections getting delivered at a faster rate than the current system is structured to deliver them.

That's where a less obvious part of the investment landscape comes in: the independent connection providers (ICPs) and the SMEs that supply, build, and operate the physical kit underneath the headline GW figures. Independents already handle the majority of new distribution-level connections in Britain, and their existence has become increasingly important because incumbent network owners, regulated on multi-year price control cycles, aren't built for speed. As ICPs grow, the pattern tends to be the same: they climb the voltage scale, taking on larger and more technically demanding connections, and in doing so they need more specialist equipment, more skilled engineering capacity, and more capital.

This is the opportunity for private investment into UK SMEs, and forms part of Connection Capital’s investment thesis: the biggest constraints, and therefore potentially the most attractive investment opportunities are in the infrastructure part of the sector, the ‘picks and shovels’, the enabling layer that every technology depends on, regardless of which one wins. Our strategy is to invest across that value chain. Not as a bet on the grid in the abstract, but on the specific businesses making and installing transformers, building substations, and operating as the connection layer between an overstretched incumbent network and a queue of impatient demand.

The UK's own experience with transformer manufacturing is a small preview of how concentrated and underbuilt this supply chain still is. Connection Capital’s 2024 investment in the £35m management buyout of Winder Power, which enabled the executive team to own and grow the business, is a live demonstration of our thesis. Winder Power is a Leed-based manufacturer of power and distribution transformers founded in 1898 that helps to keep power flowing safely through the UK network. It won six of the seven frameworks in 2024 to supply into UK Distribution Network Operators (facilitators of connections into the network) and is currently re-developing its 80,000 sq ft Leeds site to significantly expand its addressable market.

The grid the UK had in 1965 was simple with predictable energy generation from a handful of sites. The grid Britain needs by 2035 is none of those things. Turning this 283GW ambition into actual, connected capacity will depend less on any single government target than on whether enough capital reaches the specific businesses doing the physical work of plugging the country back in.

What is Connection Capital targeting next?

Connection Capital’s direct investment team targets high-growth UK businesses in the lower mid-market typically deploying equity tickets of £3m – 12m to back strong management teams in structurally underpinned markets. We're straightforward to work with, we move quickly when the fit is right, and we're transparent about our thinking from the first conversation.

If you are working with founders or management teams in grid infrastructure, battery storage, or the enabling technology layer and you're looking for a capital partner who knows this market and can move with conviction, we'd like to hear from you.